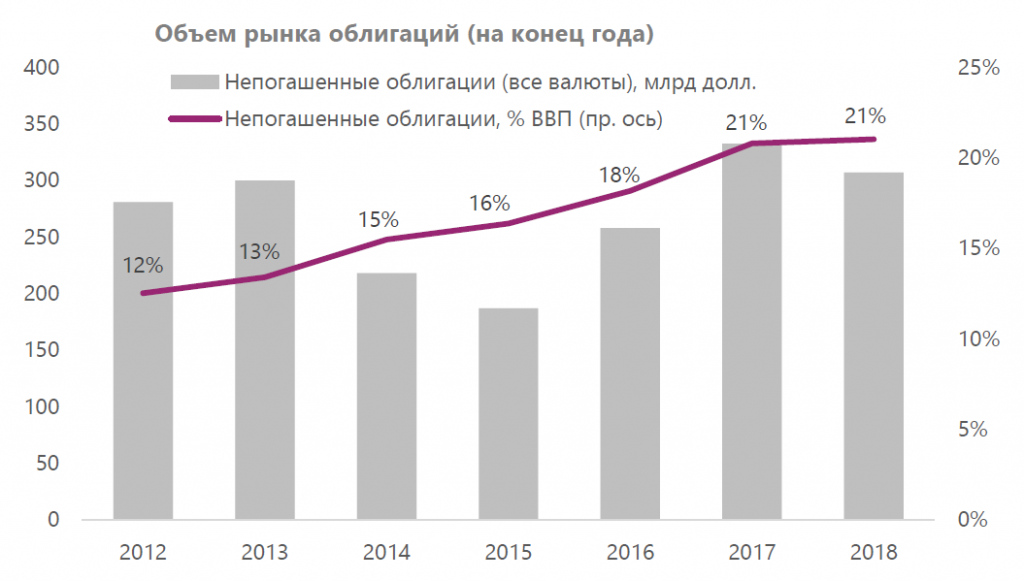

The bond market in Russia is relatively small, taking around 21% of GDP. This is partly because of a relatively high-rate interest rate environment, holding back all kinds of debt.

The bond market in Russia is steadily growing as a lower inflation environment leads to an extended planning horizon of investors and borrowers. Debt-aimed sanctions on Russian entities provide additional stimulus to borrow internally.

The biggest appetite to hold bond instruments comes from Russian commercial banks. Government bonds account for approximately half of the outstanding debt securities. The yields on them are widely used as a benchmark for privately issued bonds of companies with low credit risk. Among bonds of non-financial companies, 75% are issued by oil and gas, construction and development, and metals and mining companies.

Issued bonds are mostly nominated in rubles and typically have maturities of 4 to 6 years. Issues with maturities of more than 10 years are normally mortgage-backed or issued by infrastructure companies (or alternatively have an explicit or implicit government guarantee). Since 2017, some of the biggest financial institutions have started using very short-term papers with maturities of less than 1 month to manage liquidity. At least 20-30% of bonds have a built-in put or call option. Most coupons are fixed.

The credit risk of issuing entities in Russia can be assessed through national scale ratings provided by two national rating agencies. The ratings contain, among other things, information on inherent sectoral risk which is relatively persistent.

Systemic financial risk can be assessed with the use of financial stress indicators. Financial systems are interconnected, which can contribute to more frequent defaults on the contract payments of agents in some markets to agents in other markets. Large-scale episodes of this kind (financial crises) can lead to disruptions in economic activity in the real sector (initially due to the emergence of local liquidity crises), which makes them a focal point of consideration in Russia or any other country

The bond market in Russia is steadily growing as a lower inflation environment leads to an extended planning horizon of investors and borrowers. Debt-aimed sanctions on Russian entities provide additional stimulus to borrow internally.

The biggest appetite to hold bond instruments comes from Russian commercial banks. Government bonds account for approximately half of the outstanding debt securities. The yields on them are widely used as a benchmark for privately issued bonds of companies with low credit risk. Among bonds of non-financial companies, 75% are issued by oil and gas, construction and development, and metals and mining companies.

Issued bonds are mostly nominated in rubles and typically have maturities of 4 to 6 years. Issues with maturities of more than 10 years are normally mortgage-backed or issued by infrastructure companies (or alternatively have an explicit or implicit government guarantee). Since 2017, some of the biggest financial institutions have started using very short-term papers with maturities of less than 1 month to manage liquidity. At least 20-30% of bonds have a built-in put or call option. Most coupons are fixed.

The credit risk of issuing entities in Russia can be assessed through national scale ratings provided by two national rating agencies. The ratings contain, among other things, information on inherent sectoral risk which is relatively persistent.

Systemic financial risk can be assessed with the use of financial stress indicators. Financial systems are interconnected, which can contribute to more frequent defaults on the contract payments of agents in some markets to agents in other markets. Large-scale episodes of this kind (financial crises) can lead to disruptions in economic activity in the real sector (initially due to the emergence of local liquidity crises), which makes them a focal point of consideration in Russia or any other country